Commitment to Client Care

Commitment to Client Care Seamless Payment Processing Solutions

Seamless Payment Processing Solutions Defense and Compliance Attorneys

Defense and Compliance AttorneysSource: site

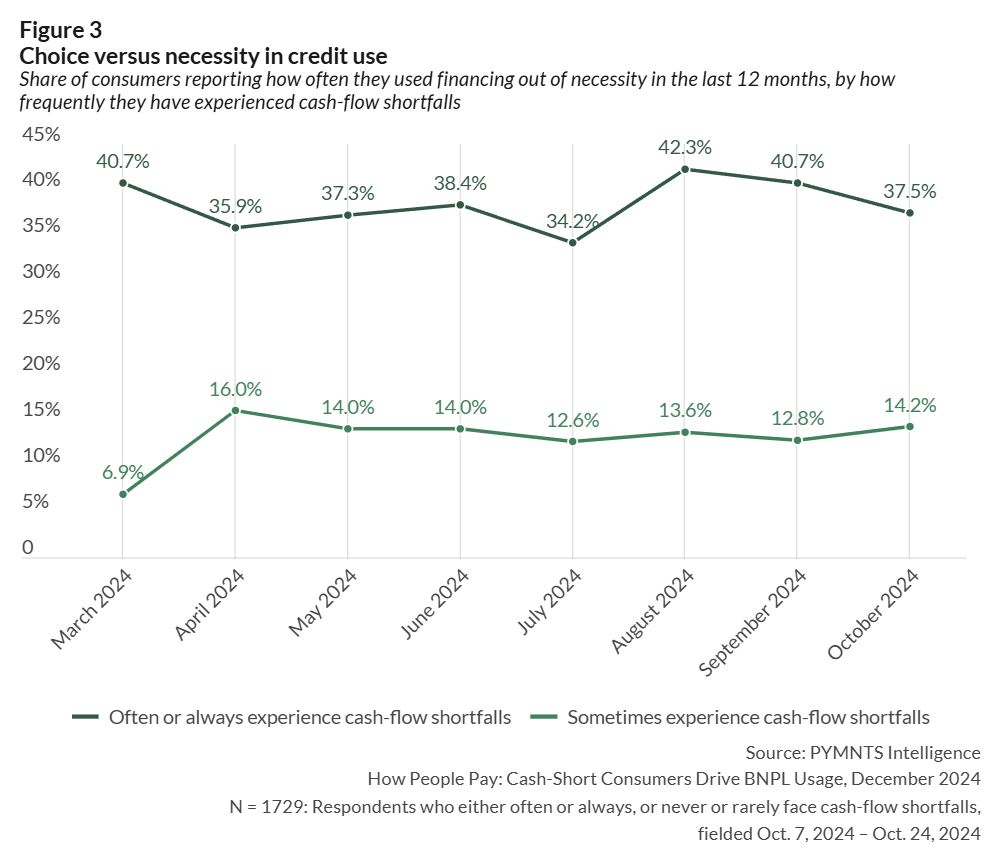

More than one-third of U.S. consumers are struggling with cash flow shortages, forcing them to make tough choices about how they pay for everyday necessities. Millennials, lower-income consumers, and those living paycheck to paycheck are especially vulnerable.

Those are some key takeaways from the recent PYMNTS Intelligence report “How People Pay: Cash-Short Consumers Drive BNPL Usage.” It’s based on a survey of 2,211 U.S. consumers conducted from Oct. 7 to 24. The survey found that consumers facing cash flow shortages are turning to alternative credit options, such as buy now, pay later (BNPL), at a much higher rate than other consumers.

Here are three big ideas from the report:

- BNPL is bridging the gap for cash-strapped consumers. Consumers with cash flow shortages are 3.5 times more likely to use BNPL than consumers who are financially stable. Meanwhile, 8.9% of consumers who frequently experience cash flow shortages used BNPL in the past 30 days, compared to just 2.5% of financially stable consumers. BNPL is more accessible than traditional credit, allowing consumers to manage their financial demands without the restrictions of conventional credit.

- Millennials, lower-income consumers, and those living paycheck to paycheck are most impacted by cash flow shortages. More than one-third (35%) of consumers experience cash flow shortages. Millennials are the most affected generation, with 17% experiencing frequent cash flow issues. By comparison, only 6.6% of baby boomers and seniors reported frequent cash flow shortages. The disparity is even greater when looking at income: 18% of consumers making less than $50,000 a year report frequent cash flow shortages, while only 9.9% of those making over $100,000 said the same. Those living paycheck to paycheck are also significantly more likely to report cash flow problems.

- Credit is a necessity, not a choice, for many cash-short consumers. Consumers experiencing financial strain are more than twice as likely to use credit out of necessity. Thirty-eight percent of those frequently experiencing cash flow shortages said they use credit out of necessity, compared to just 14% of financially stable consumers. However, those who need credit the most often face the greatest barriers to access. Financially constrained consumers are less likely to use credit cards for retail and grocery purchases than the broader sample. Limited access to traditional credit is driving many consumers to turn to BNPL to get through cash shortages.

As the report concluded: “Paradoxically, those who need credit the most often face the greatest barriers to accessing it. Many consumers are not able get credit due to bad or no credit history. Also the high cost of credit can be a barrier for struggling consumers. For financially constrained individuals, only 17% made retail and 16% made grocery purchases using credit cards, compared to an average of 34% for retail and 30% for groceries among the broader sample. Limited access drives many to rely on alternative credit options like BNPL to get through cash shortages. While traditional credit remains a vital resource for some, others need to turn to innovative alternatives to navigate financial constraints.”

Upcoming Events

Seamless Payment Processing Solutions

Seamless Payment Processing Solutions